My Toshiba experience as “Head of Supply Chain and Planning” in the Notebook Division for the Emerging-EMEA markets during the economic crisis 2007/2008

The 2007-2008 financial crisis presented a natural learning environment about competitive advantage, demonstrating the strategic value of early warning systems, supply chain agility, and rapid organizational response.

Outcome: Our BU was stabilizing the European profit situation and earning the global President’s Award.

This assessment provides a qualified and quantified evaluation of demonstrated leadership competencies suitable for any executive-level.

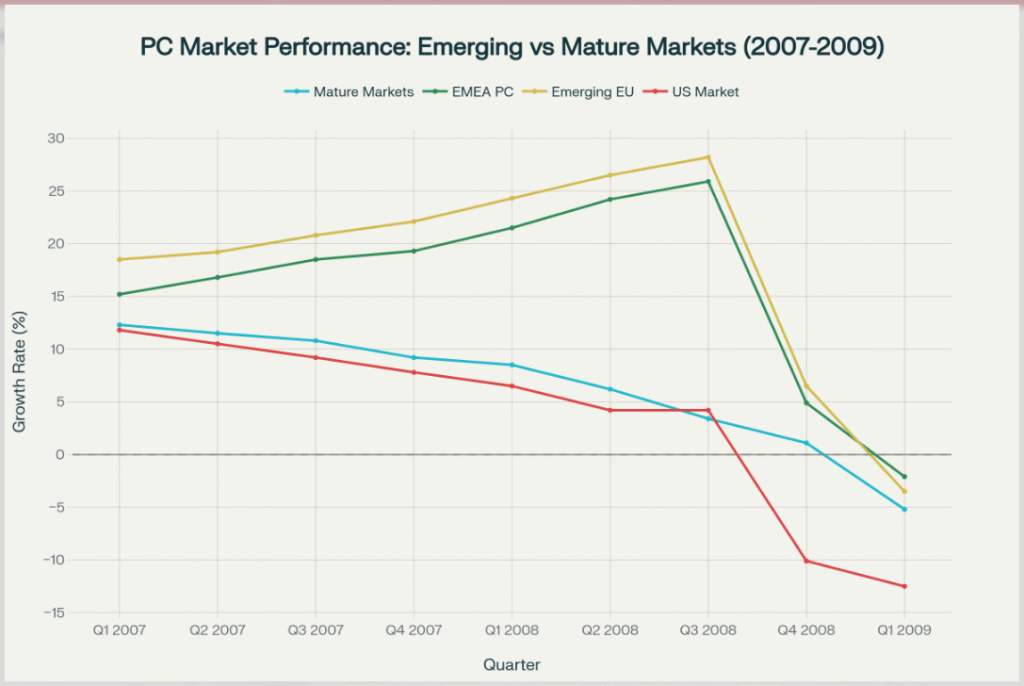

At a glance, the overall PC/Notebook market development from 2007 to 2009:

Financial Causes of Demand Dynamics:

The 2007-2008 crisis revealed fundamental asymmetries in how financial shocks were creating different demand trajectories that sophisticated operators could have exploit:

- Mature markets—particularly the United States, Western Europe, and Japan—experienced direct exposure to the financial system collapse originating in subprime mortgage markets. Their banking systems held toxic assets worth trillions of dollars, credit markets froze completely in September-October 2008, and highly leveraged consumers faced simultaneous wealth destruction through collapsing home values and equity portfolios.

In the United States, household debt-to-income ratios had reached 130% by 2007, supported by easy credit and rising asset prices. When housing prices fell 30-40% nationally and credit availability evaporated overnight, consumers had no choice but to slash spending, particularly on discretionary items like technology products.

- The PC market in mature economies reflected this dynamic: US market growth decelerated from 11.8% in Q1 2007 to -12.5% by Q1 2009, while overall mature market growth collapsed from 12.3% to -5.2% over the same period.

Three structural factors explain the Emerging Markets development, all documented extensively in International Monetary Fund and World Bank crisis analyses.

- In many financial systems minimal exposure was recognized in comparison to the complex derivatives and securitized products that amplified losses in developed economies.

- In Europe for example bank practice in Poland, Czech Republic, and Romania did not engage that strong in the subprime lending practices or created the mortgage-backed securities that devastated Western institutions.

- Emerging market growth trajectories were often different from mature economies, driven more by catch-up economic development and productivity gains rather than credit-fueled consumption.

- Poland’s economy, for example, continued growing at 5.1% in 2008 and 1.6% in 2009—the only EU member to avoid recession—because its growth stemmed from improving productivity, EU structural fund investments, and expanding exports rather than household debt accumulation.

- Exceptions like Dubai will follow below and will have a critical impact as early warning system through market portfolio management.

- Many emerging markets—particularly Poland, Czech Republic, and select MEA countries—had implemented sound macroeconomic policies in the years preceding the crisis, maintaining fiscal discipline and avoiding the current account deficits that created vulnerability elsewhere.

Three things to be anchored before crisis appears:

- Investment strategies, enabling proactive decision-making through Integrated Business Planning (IBP) processes that distribute strategic decision-making authority

- Supply chain flexibility enabling lead time advantages

- Regional/global product-portfolio advantages supporting last minute production changes on critical components; to support monthly/weekly regional warning calls for greater crisis resilience

- FI/CO insights: Close coordination on financially driven stock/inventory Sell-Out situations; measuring both inhouse and customer level. – Lagging payments become most critical KPI stopping deliveries; recreating product volumes and customer allocation sheets with asap alignment with Sales teams to re-route volumes.

These pattern are creating a reduction in team- and leadership pressure, enabling faster and more resilient responses when disruptions occur.

The “Third Family-Notebook” Phenomenon:

A discretionary spending factor as emerging markets leading crisis indicator

The collapse of “third notebook” demand provided for our IBP-team the first critical early warning signal in 2007 as the apex of discretionary consumer spending:

- Research on consumer behavior during economic crises consistently demonstrates that discretionary purchases—particularly for higher-order goods representing surplus consumption—decline first and most dramatically when financial stress emerges.

Results:

- As a first responder to the upcoming crisis and a flexible supply chain with sea and air shipment in combination with the factors mentioned above, we were maintaining a very stable demand and supply situation.

- All regional teams were supporting each other if re-allocation of products was obliged and/or profit sharing was necessary, as sometimes certain products could not be absorbed by originally planned/allocated customers.

Why Emerging Markets Collapsed in 2009

By Q4 2008 to Q1 2009, the global economic collapse reached also the Emerging markets through several transmission channels:

- Credit crunch and capital flight: After the Lehman Brothers collapse, global liquidity dried up, foreign direct investment and export earnings plummeted, and consumer credit disappeared.

- Falling GDP and employment: The IMF and World Bank reported sharp slowdowns in emerging markets’ GDP, reducing household purchasing power and corporate IT budgets.

- Corporate and consumer caution: Both users and firms extended PC replacement cycles. Gartner noted that “users stretch PC lifetimes and suppliers grow increasingly cautious,” which sharply curbed shipments.

- Inventory contraction: Manufacturers and distributors deliberately cut inventories to avoid overstocking during economic uncertainty, leading to plunging shipment numbers even where latent demand existed.

Structural Industry Factors

Finally, internal market dynamics worsened the downturn:

- Rapid price erosion from competition in the low-end (netbook) segment slashed revenues despite unit growth.

- Shifts toward cheaper, underpowered devices delayed high-margin replacement cycles.

- Global semiconductor and supply chain contraction, with chip sales dropping 9% in 2009, limited manufacturing continuity.

In summary, emerging markets fell later but the Forecast assumed by our teams moved the volume-downturn in the same way as explained above.